Put Bear Spread indicatorPut bear spread indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a DEBIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

- Put spread price (Debit): The debit paid for one unit of options strategy.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-% of Max Profit/Loss: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (0.95).

Example: In this spread, -0.95 means, 95% of the options strategy maximum loss is reached and, 0.95 means, 95% of the options strategy maximum profit is reached.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Pesquisar nos scripts por "Implied volatility"

Iron Condor / butterfly buy or sell indicatorIron Condor / butterfly indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Buy or sell (the strategy)

- Iron Condor price bought/sold: enter the price that you bought/sold one options strategy.

-Instrument price when bought/sold: the stock price when you bought/sold the options strategy.

-Upper strike price Top: the top upper strike price of the options strategy.

-Lower strike price Top: the top lower strike price of the options strategy.

-Upper strike price Bottom: the bottom upper strike price of the options strategy.

-Lower strike price Bottom: the bottom lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-% of Profit/Loss: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (0.95).

Example: If the strategy was bought, -0.95 means, 95% of the options strategy maximum loss is reached. : If the strategy was bought, 0.95 means, 95% of the options strategy maximum profit is reached.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Straddle / strangle buy or sell indicatorStraddle / strangle buy or sell indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Buy or sell (the strategy)

- Straddle/strangle price bought/sold: enter the price that you bought/sold one options strategy.

-Instrument price when bought/sold: the stock price when you bought/sold the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-Risk to reward: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (3).

Example: If the strategy was bought, -0.95 means, 95% of the options strategy value is lost (unrealized). If the strategy was bought, 3 means, the risk to reward is 3.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Call Bear Spread indicatorCall bear spread indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a CREDIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

- Call spread price (Credit): The credit received for one unit of options strategy.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-% of Max Profit/Loss: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (0.95).

Example: In this spread, -0.95 means, 95% of the options strategy maximum loss is reached and, 0.95 means, 95% of the options strategy maximum profit is reached.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Call bull spread indicatorCall bull spread indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a DEBIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

- Call spread price (Debit): The debit paid for one unit of options strategy.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-% of Max Profit/Loss: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (0.95).

Example: In this spread, -0.95 means, 95% of the options strategy maximum loss is reached and, 0.95 means, 95% of the options strategy maximum profit is reached.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Put option buy or sell indicatorPut option indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Buy or sell (the strategy)

-The option price bought: at what price did you bought/sold one option.

-Instrument price when bought: the stock price when you bought/sold the option.

-Strike price: the strike price of the option.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-Risk to reward: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (3).

Example: If an option was bought, -0.95 means, 95% of the option value is lost (unrealized). If an option was bought, 3 means, the risk to reward is 3.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Call option buy or sell indicatorCall option indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Buy or sell (the strategy)

-The option price bought: at what price did you bought/sold one option.

-Instrument price when bought: the stock price when you bought/sold the option.

-Strike price: the strike price of the option.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-Risk to reward: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (3).

Example: If an option was bought, -0.95 means, 95% of the option value is lost (unrealized). If an option was bought, 3 means, the risk to reward is 3.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Improved Historical Volatility Calculator (No Options)Improved Historical Volatility Calculator (No Options)

Description

The "Improved Historical Volatility Calculator (No Options)" is a Pine Script indicator designed to calculate the historical volatility (HV) of assets without relying on options data. This tool is particularly useful for markets like forex, indices, or stocks where options trading might be limited or unavailable. It provides a customizable way to measure volatility based on historical price movements, with options to adjust the calculation period, trading days per year, and use an exponentially weighted moving average (EWMA) for enhanced sensitivity to recent data.

This indicator can be used standalone to visualize volatility trends or integrated with other scripts (e.g., option pricing models) to provide a manual input for implied volatility (IV).

Features

Customizable Period: Adjust the number of days (5 to 365) for volatility calculation.

Flexible Annualization: Set the number of trading days per year (default 252) to suit different markets (e.g., 365 for forex).

EWMA Option: Toggle between standard deviation and EWMA for a more responsive volatility measure.

Trend Adjustment: Removes the influence of price trends using an EMA-based detrending method.

Visual Output: Displays volatility as a histogram and labels the latest value on the chart.

How to Use

Add the Indicator: Load the indicator onto your chart via the Pine Script editor or the Indicators menu.

Configure Settings:

Period for Calculation: Set the lookback period (e.g., 30 days) to calculate volatility.

Trading Days per Year: Adjust for your market (e.g., 252 for stocks, 365 for continuous markets).

Use EWMA: Enable for a weighted approach focusing on recent volatility.

Interpret the Results: The histogram shows volatility in decimal form (e.g., 0.03136 = 3.136%), and the label displays the percentage on the last bar.

Integration: Use the calculated volatility value (in decimal form) as a manual IV input in other scripts, such as option pricing models.

Example

For the DXY index, with a 60-day period and 252 trading days per year, the indicator might output a volatility of 0.03136 (3.136%). You can input this value into an options model to estimate standard deviation levels, adjusting for the days to expiry.

Notes

Accuracy: The indicator provides a reliable estimate of historical volatility, with improvements like trend removal and EWMA. For precision, use a period that matches your trading horizon (e.g., 30-90 days).

Limitations: Volatility is based on historical data and may not reflect future market conditions or implied volatility from options.

Compatibility: Tested on TradingView as of June 16, 2025. Ensure sufficient historical data is available for the chosen period.

Suggestions

Increase the period for volatile assets to smooth out noise.

Share feedback or request enhancements in the comments!

Black-Scholes Model CalculatorOverview

The Black-Scholes Model Calculator TradingView Indicator is an advanced tool designed for options traders to calculate key Greek values, including Theta, Gamma, Delta, Rho, and Vega. By integrating this indicator into your TradingView charts, you can perform sophisticated options analysis, enhance your understanding of options pricing, and make more informed trading decisions.

Key Features

1. Comprehensive Greeks Calculation:

Theta : Measure the sensitivity of the option's price to the passage of time, helping you understand time decay.

Gamma : Determine the rate of change of Delta, providing insights into how Delta will change as the underlying asset price moves.

Delta : Calculate the sensitivity of the option's price to changes in the price of the underlying asset.

Rho : Evaluate the sensitivity of the option's price to changes in interest rates.

Vega : Assess the sensitivity of the option's price to changes in implied volatility.

2. User Input Parameters :

Strike Price : Enter the strike price of the option to tailor the calculations to your specific option.

Days Remaining : Input the number of days remaining until the option's expiration, providing accurate time-based calculations.

Implied Volatility (IV) : Specify the implied volatility for both call and put options to reflect market expectations.

3. Visual and Analytical Insights :

Display the calculated Greek values directly on your TradingView chart for quick reference and analysis.

Clear and intuitive presentation of the data, making it easy to interpret and apply to your trading strategy.

How to Use

1. Insert Strike Price : Start by entering the strike price of the option you are analyzing. This is essential for calculating the Greeks accurately.

2. Days Remaining : Input the number of days left until the option's expiration. This factor is crucial for determining Theta and other time-sensitive Greeks.

3. Implied Volatility (IV) : Provide the implied volatility values for both call and put options. This input is vital for calculating Vega and assessing how changes in volatility affect option prices.

Benefits

Enhanced Options Trading : Gain a deeper understanding of how different factors affect option pricing by using the calculated Greeks.

Strategic Planning : Utilize the Greek values to formulate and adjust your options trading strategies based on time decay, price movements, interest rate changes, and volatility shifts.

Risk Management : Improve your risk management by understanding the potential changes in option prices and adjusting your positions accordingly.

Practical Application

1. Theta Management : Monitor Theta to understand how time decay is impacting your option positions, especially for short-term trades.

2. Gamma and Delta Adjustments : Use Gamma and Delta to hedge your positions and manage the risk associated with price movements in the underlying asset.

3. Rho Considerations : Evaluate Rho to factor in interest rate changes, which can be particularly useful in long-term options trading.

4. Vega Analysis : Analyze Vega to assess the impact of volatility changes and adjust your strategies in volatile market conditions.

Conclusion

The Black-Scholes Model Calculator TradingView Indicator is an indispensable tool for any serious options trader. By providing precise calculations of Theta, Gamma, Delta, Rho, and Vega, it empowers you to make more informed trading decisions, manage risks effectively, and optimize your options trading strategies. Integrate this indicator into your TradingView setup to take your options trading to the next level.

NSE BSE Option Chain with Greeks [Bluechip Algos]This indicator provides option chain information along with greeks of Delta, Vega, Theta, Gamma and Rho.

Make sure inputs are correctly entered; Symbol, reference spot price of ATM, Expiry date and Distance between strikes

Here’s a brief explanation of the logic used for calculating the Greeks in your Pine Script:

Implied Volatility (IV):

Implied Volatility is found using Black-Scholes formula by comparing the market price of the option to its theoretical price. An iterative process is used to adjust the volatility value until the theoretical price matches the market price, effectively reversing the pricing model to deduce the market’s expectation of volatility.

Delta:

Delta is calculated by estimating the probability of the option expiring in the money. This probability is derived using statistical methods based on price movement expectations. It is computed using the cumulative normal distribution function normDist

Gamma:

Gamma is calculated by evaluating how Delta changes when the underlying price moves slightly, giving a sense of the stability of Delta across different price levels. It is computed based on the derivative of Delta concerning the spot price

Theta:

Theta calculates the time decay of an option's value. It estimates how much the option's price will reduce as it gets closer to expiry, assuming all other factors remain constant. For this, the time left to expiry is broken into daily increments to assess the decay rate.

Vega:

Vega is determined by analyzing how the option's price would react to changes in market volatility. It uses the relationship between volatility and option pricing to measure this sensitivity, helping traders understand the impact of fluctuating volatility levels.

Rho:

Rho is calculated by estimating how much the option's price would change for a small increase in the risk-free interest rate. The calculation involves using Black-Scholes to assess how interest rate changes alter the discounted value of the option's payoff.

All computations depend on parameters like the spot price S, strike price X, time to expiry t, risk-free rate r, and volatility σ.

Implied and Historical Volatility v4There is a famous option strategy📊 played on volatility📈. Where people go short on volatility, generally, this strategy is used before any significant event or earnings release. The basic phenomenon is that the Implied Volatility shoots up before the event and drops after the event, while the volatility of the security does not increase in most of the scenarios. 💹

I have tried to create an Indicator using which you

can analyse the historical change in Implied Volatility Vs Historic Volatility.

To get a basic idea of how the security moved during different events.

Notes:

a) Implied Volatility is calculated using the bisection method and Black 76 model option pricing model.

b) For the risk-free rate I have fetched the price of the “10-Year Indian Government Bond” price and calculated its yield to be used as our Risk-Free rate.

historical volatility by flashThe script is made to help to determine OPTIONS volatility.

The Script is showing the Historical volatility of any stock for its last 1 year data.

Historical volatility is important to know how stock can perform in panic days.

Historical volatility is best used with Implied volatility.

How to Interpret the Script or How to use it?

The Script show 5 parts the lowermost is lowest HV in last year & the highest part shows highest volatility in the past 1 year.

Use this on a DAILY CHART only.

Now Take the IV (implied volatility of stock) and put that figure in between the HV and check in which part current IV resides. based on that you can determine how OPTIONS premium or how much it INFLATED or DEFLATED .

Standard Deviation Levels with Settlement Price and VolatilityStandard Deviation Levels with Settlement Price and Volatility.

This indicator plots the standard deviation levels based on the settlement price and the implied volatility. It works for all Equity Stocks and Futures.

For Futures

Symbol Volatility Symbol (Implied Volatility)

NQ VXN

ES VIX

YM VXD

RTY RVX

CL OVX

GC GVZ

BTC DVOL

The plot gives you an ideas that the price has what probability staying in the range of 1SD,2SD,3SD ( In normal distribution method)

Please provide the feedback or comments if you find any improvements

Steamroom Levels V3 - Dynamic IVOptions flow visualization tool displaying Gamma Exposure (GEX) levels and IV-derived pivot levels with intelligent auto-timeframe selection.

Overview

Steamroom Levels V3 visualizes two components of options market structure on your chart: Gamma Exposure (GEX) levels and Steamroom Pivots. These levels are derived from derivatives market data and help traders identify potential support, resistance, and expected price ranges based on options positioning and implied volatility.

Core Components

Gamma Exposure (GEX) Levels

Gamma Exposure represents aggregate options positioning at various strike prices. When market makers sell options, they hedge their exposure by buying or selling the underlying asset. This hedging activity can create predictable price behavior around key strike levels.

Four GEX level types are displayed:

Put Wall (Major) : The strike with the highest concentration of put gamma. As price approaches, dealer hedging may create buying pressure, often acting as support.

Put Wall Minor : Secondary put gamma concentrations providing interim support zones.

Call Wall (Major) : The strike with the highest concentration of call gamma. Dealer hedging may create selling pressure as price rises toward this level, often acting as resistance.

Call Wall Minor : Secondary call gamma concentrations providing interim resistance zones.

Steamroom Pivots

Steamroom Pivots are support and resistance levels calculated using implied volatility data from the options market. The calculation method works as follows:

Methodology:

The indicator takes the selected IV timeframe value (1-day, 5-day, 30-day, or 90-day implied volatility expressed as a decimal)

Three proprietary multipliers are applied to this IV value to create bands above and below the anchor price

The previous daily close serves as the anchor point

This produces three resistance levels (R1, R2, R3) above the anchor and three support levels (S1, S2, S3) below

The Six Pivot Levels:

R1 / S1 – Nearest pivot levels; represent the first reaction zones

R2 / S2 – Extended pivot levels; secondary targets

R3 / S3 – Outer pivot levels; represent significant price extensions

The specific multipliers used are calibrated based on observed market behavior and are not disclosed, but the general approach uses implied volatility as a measure of expected price movement scaled to create meaningful intraday and swing trading levels.

Auto IV Timeframe Selection

The indicator automatically selects the appropriate implied volatility timeframe based on your chart's timeframe. This ensures pivot levels remain relevant to your trading horizon.

Default Auto Behavior:

Chart Timeframe IV Selected

Up to 30 minutes 1-day IV

31 minutes to 4 hours 5-day IV

4 hours to 1 week 30-day IV

Above 1 week 90-day IV

Customizable Thresholds:

You can adjust these cutoffs in the settings:

"Auto: 1-day IV up to (min)" – Default: 30

"Auto: 5-day IV up to (min)" – Default: 240 (4 hours)

"Auto: 30-day IV up to (min)" – Default: 10080 (1 week)

Manual Override:

Select 1-day, 5-day, 30-day, or 90-day directly to lock in a specific IV timeframe regardless of chart timeframe.

Info Table

An on-chart table displays the currently active IV timeframe. When using Auto mode, it shows which IV was selected (e.g., "IV: 1-day IV (Auto)").

Table Settings:

Show/Hide toggle

Position: Top Left (default), Top Right, Bottom Left, Bottom Right, Top Center, or Bottom Center

Text size: Tiny, Small, Normal, Large, Huge

Text and background color customization

Data Input

This indicator requires external data input. Paste your formatted data string into the "Paste V3 Data" field in settings. The indicator automatically matches data to the current chart symbol.

The data format supports multiple symbols simultaneously. Only levels matching the active chart are displayed.

How To Use

GEX Levels

Put Wall levels may act as support; Call Wall levels may act as resistance

Minor walls provide interim reaction zones

Breaks through major walls may indicate momentum shifts

Steamroom Pivots

R1/S1 are the nearest pivot levels – common intraday reaction points

R2/S2 serve as extended targets

R3/S3 mark outer boundaries for significant moves

Confluence between GEX levels and pivots strengthens a price zone's significance

Customization Options

GEX Settings

Toggle visibility for levels and labels

Show/hide prices in labels

Line extension direction

Label size and offset

Pivot Settings

Toggle visibility for levels and labels

Show/hide prices in labels

IV timeframe selection (Auto or manual)

Auto threshold customization

Line extension direction

Label size and offset

Styling

Independent colors for Put Wall, Put Minor, Call Wall, Call Minor

Line styles: Solid, Dotted, Dashed

Line width: 1-4 pixels

Pivot color with independent styles per level pair (R1/S1, R2/S2, R3/S3)

Technical Notes

Multi-symbol data supported; only matching symbol levels are displayed

Pivots anchor to the confirmed daily close

Auto IV selection uses native TradingView timeframe detection

Visual elements are efficiently managed and cleaned up on each update

Disclaimer

This indicator is for informational and educational purposes only. Displayed levels are based on options market data and do not guarantee future price behavior. Past performance is not indicative of future results. Always conduct your own analysis and manage risk appropriately. Trading involves substantial risk of loss.

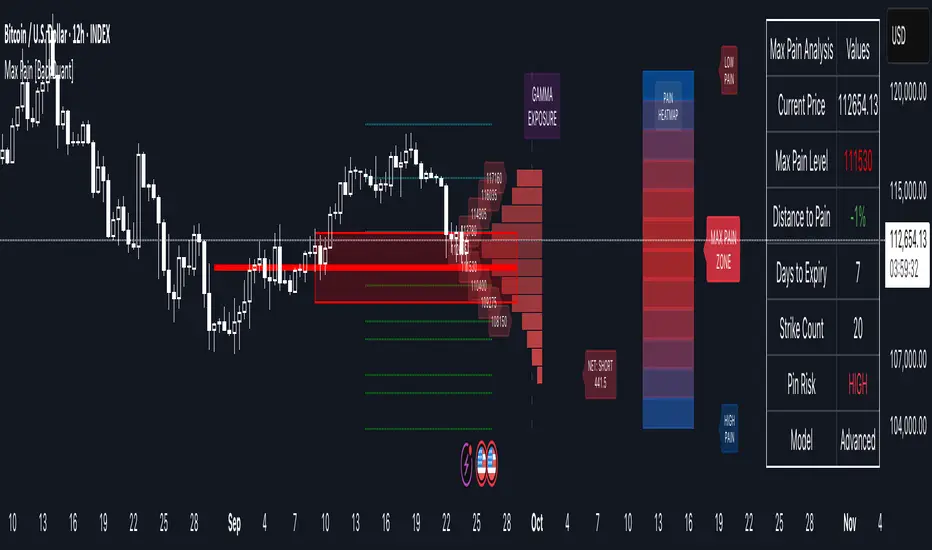

Options Max Pain Calculator [BackQuant]Options Max Pain Calculator

A visualization tool that models option expiry dynamics by calculating "max pain" levels, displaying synthetic open interest curves, gamma exposure profiles, and pin-risk zones to help identify where market makers have the least payout exposure.

What is Max Pain?

Max Pain is the theoretical expiration price where the total dollar value of outstanding options would be minimized. At this price level, option holders collectively experience maximum losses while option writers (typically market makers) have minimal payout obligations. This creates a natural gravitational pull as expiration approaches.

Core Features

Visual Analysis Components:

Max Pain Line: Horizontal line showing the calculated minimum pain level

Strike Level Grid: Major support and resistance levels at key option strikes

Pin Zone: Highlighted area around max pain where price may gravitate

Pain Heatmap: Color-coded visualization showing pain distribution across prices

Gamma Exposure Profile: Bar chart displaying net gamma at each strike level

Real-time Dashboard: Summary statistics and risk metrics

Synthetic Market Modeling**

Since Pine Script cannot access live options data, the indicator creates realistic synthetic open interest distributions based on configurable market parameters including volume patterns, put/call ratios, and market maker positioning.

How It Works

Strike Generation:

The tool creates a grid of option strikes centered around the current price. You can control the range, density, and whether strikes snap to realistic market increments.

Open Interest Modeling:

Using your inputs for average volume, put/call ratios, and market maker behavior, the indicator generates synthetic open interest that mirrors real market dynamics:

Higher volume at-the-money with decay as strikes move further out

Adjustable put/call bias to reflect current market sentiment

Market maker inventory effects and typical short-gamma positioning

Weekly options boost for near-term expirations

Pain Calculation:

For each potential expiry price, the tool calculates total option payouts:

Call options contribute pain when finishing in-the-money

Put options contribute pain when finishing in-the-money

The strike with minimum total pain becomes the Max Pain level

Gamma Analysis:

Net gamma exposure is calculated at each strike using standard option pricing models, showing where hedging flows may be most intense. Positive gamma creates price support while negative gamma can amplify moves.

Key Settings

Basic Configuration:

Number of Strikes: Controls grid density (recommended: 15-25)

Days to Expiration: Time until option expiry

Strike Range: Price range around current level (recommended: 8-15%)

Strike Increment: Spacing between strikes

Market Parameters:

Average Daily Volume: Baseline for synthetic open interest

Put/Call Volume Ratio: Market sentiment bias (>1.0 = bearish, <1.0 = bullish) It does not work if set to 1.0

Implied Volatility: Current option volatility estimate

Market Maker Factors: Dealer positioning and hedging intensity

Display Options:

Model Complexity: Simple (line only), Standard (+ zones), Advanced (+ heatmap/gamma)

Visual Elements: Toggle individual components on/off

Theme: Dark/Light mode

Update Frequency: Real-time or daily calculation

Reading the Display

Dashboard Table (Top Right):

Current Price vs Max Pain Level

Distance to Pain: Percentage gap (smaller = higher pin risk)

Pin Risk Assessment: HIGH/MEDIUM/LOW based on proximity and time

Days to Expiry and Strike Count

Model complexity level

Visual Elements:

Red Line: Max Pain level where payout is minimized

Colored Zone: Pin risk area around max pain

Dotted Lines: Major strike levels (green = support, orange = resistance)

Color Bar: Pain heatmap (blue = high pain, red = low pain/max pain zones)

Horizontal Bars: Gamma exposure (green = positive, red = negative)

Yellow Dotted Line: Gamma flip level where hedging behavior changes

Trading Applications

Expiration Pinning:

When price is near max pain with limited time remaining, there's increased probability of gravitating toward that level as market makers hedge their positions.

Support and Resistance:

High open interest strikes often act as magnets, with max pain representing the strongest gravitational pull.

Volatility Expectations:

Above gamma flip: Expect dampened volatility (long gamma environment)

Below gamma flip: Expect amplified moves (short gamma environment)

Risk Assessment:

The pin risk indicator helps gauge likelihood of price manipulation near expiry, with HIGH risk suggesting potential range-bound action.

Best Practices

Setup Recommendations

Start with Model Complexity set to "Standard"

Use realistic strike ranges (8-12% for most assets)

Set put/call ratio based on current market sentiment

Adjust implied volatility to match current levels

Interpretation Guidelines:

Small distance to pain + short time = high pin probability

Large gamma bars indicate key hedging levels to monitor

Heatmap intensity shows strength of pain concentration

Multiple nearby strikes can create wider pin zones

Update Strategy:

Use "Daily" updates for cleaner visuals during trading hours

Switch to "Every Bar" for real-time analysis near expiration

Monitor changes in max pain level as new options activity emerges

Important Disclaimers

This is a modeling tool using synthetic data, not live market information. While the calculations are mathematically sound and the modeling realistic, actual market dynamics involve numerous factors not captured in any single indicator.

Max pain represents theoretical minimum payout levels and suggests where natural market forces may create gravitational pull, but it does not guarantee price movement or predict exact expiration levels. Market gaps, news events, and changing volatility can override these dynamics.

Use this tool as additional context for your analysis, not as a standalone trading signal. The synthetic nature of the data makes it most valuable for understanding market structure and potential zones of interest rather than precise price prediction.

Technical Notes

The indicator uses established option pricing principles with simplified implementations optimized for Pine Script performance. Gamma calculations use standard financial models while pain calculations follow the industry-standard definition of minimized option payouts.

All visual elements use fixed positioning to prevent movement when scrolling charts, and the tool includes performance optimizations to handle real-time calculation without timeout errors.

Ichimoku Z-Score Stochastic Oscillator with Kumo Depth Analysis---

Ichimoku Z-Score Stochastic Oscillator with Kumo Depth Analysis

---

Script Overview

Welcome to the Advanced Ichimoku Z-Score Stochastic Oscillator with Kumo Depth Analysis. This unique strategy is designed to provide a comprehensive, multi-timeframe trading view by leveraging the Ichimoku Cloud, Z-Score, Stochastic Oscillator, and an innovative implied volatility measure – the Kumo Depth. By integrating these powerful tools into one script, traders can make more informed decisions by considering trend strength, volatility, and volume in one holistic view.

Rationale & Strategy

The script was created with the rationale that trading decisions should not only be based on price action and volume, but also on market trend strength and implied volatility. The script integrates these various elements:

The Ichimoku Cloud, a versatile indicator that provides support and resistance levels, trend direction, and momentum all at once.

The Z-Score, a statistical measurement of a value's relationship to the mean (average) of a group of values.

The Stochastic Oscillator, a momentum indicator that uses support and resistance levels to determine probable trend reversals.

The Kumo Depth Analysis, an innovative measure of implied volatility and market trend strength derived from the thickness of the Ichimoku Cloud.

How It Works

This script works by providing visual buy and sell signals based on the confluence of the aforementioned tools.

Ichimoku Cloud and Z-Score: The script first calculates the Ichimoku Cloud lines for both a higher and lower timeframe and measures how much current prices deviate from the cloud using Z-Score.

Stochastic Oscillator: This Z-Score is then inputted into a Stochastic Oscillator, thus giving the oscillator a more normalized range.

Kumo Depth Analysis: Simultaneously, the thickness of the Ichimoku Cloud (Kumo) is calculated as an implied volatility indicator. This depth is normalized and used as a filter to ensure we are trading in a market with substantial trend strength.

Signals: Buy and sell signals are triggered based on the crossover and crossunder of the Stochastic Oscillator lines. Signals are then filtered based on their location relative to the Ichimoku Cloud (price should be above the cloud for buy signals and below for sell signals) and the normalized Kumo Depth.

How to Use

Signal Types: The script provides both strong and weak signals. Strong signals are accompanied by high volume, while weak signals are not. Strong buy signals are indicated with a green triangle at the top, strong sell signals with a red triangle at the bottom. Weak signals are shown as blue and yellow circles, respectively.

Trend Strength: The trend strength is shown by the normalized Kumo Depth. The greater the Kumo Depth, the stronger the trend.

Timeframes: You can customize the timeframes used for the calculations in the input settings.

Adjustments: Users can adjust parameters such as the Ichimoku settings, Stochastic Oscillator settings, timeframes, and Kumo Depth settings to suit their trading style and the characteristics of the asset they are trading.

This script is a complete trading strategy tool providing multi-timeframe, trend-following, and volume-based signals. It's best suited for traders who understand the concepts of trend trading, stochastic oscillators, and volatility measures and want to incorporate them all into one powerful, comprehensive trading strategy.

Cash VIX Term StructureLet’s first start with some definitions:

VIX9D: The CBOE S&P 500 9-Day Volatility Index estimates the expected 9-day volatility of S&P 500® stock returns.

www.cboe.com

VIX: The CBOE Volatility Index® (VIX® ) is considered by many to be the world's premier barometer of equity market volatility. The VIX Index is based on real-time prices of options on the S&P 500® Index (SPX) and is designed to reflect investors' consensus view of future (30-day) expected stock market volatility. The VIX Index is often referred to as the market's "fear gauge".

www.cboe.com

VIX3M: The CBOE 3-Month Volatility Index is designed to be a constant measure of 3-month implied volatility of the S&P 500® (SPX) Index options.

www.cboe.com

VIX6M: The CBOE S&P 500 6-Month Volatility Index is an estimate of the expected 6-month volatility of the S&P 500® Index.

www.cboe.com

VIX1Y: The CBOE S&P 500 1-Year Volatility Index is an estimate of the expected 1-Yeaer volatility of the S&P 500® Index.

www.cboe.com

This indicator visually displays the relationship between all the above products (short term vol vs long term vol). It also displays the current value and daily percentage change.

The shape of the term structure can tell us a lot about the market:

When the slope of the term structure is upward sloping (longer term VIX are higher than shorter term VIX), we say the term structure is in contango. This usually means that market is stable.

When the slope of the term structure is downward sloping (longer term VIX are lower than shorter term VIX), we say the term structure is in backwardation. This usually happens in periods of extreme market volatility.

Sometimes VIX9D will be higher than VIX but the rest of the curve is in contango. This means that there might be some event in the next 9 days that we need to pay attention to.

I also added a few ratios that I personally track like VIX9D/VIX, VIX/VIX3M and VIX/VIX6M.

When trading short term, I tend to focus on the front end of the curve. When trading long term, I tend to look at VIX/VIX6M.

In addition to the ratios, I added some historical parameters (lookback date can be set from the indicator’s settings) like Highest Value, Lowest Value, Percentile Rank, Average, Median and Mode.

Percentile ranks are displayed for both individual products and their ratios (that’s how I like to see them).

I hope you guys like this indicator.

Happy trading!

Volatility IndicatorThe volatility indicator presented here is based on multiple volatility indices that reflect the market’s expectation of future price fluctuations across different asset classes, including equities, commodities, and currencies. These indices serve as valuable tools for traders and analysts seeking to anticipate potential market movements, as volatility is a key factor influencing asset prices and market dynamics (Bollerslev, 1986).

Volatility, defined as the magnitude of price changes, is often regarded as a measure of market uncertainty or risk. Financial markets exhibit periods of heightened volatility that may precede significant price movements, whether upward or downward (Christoffersen, 1998). The indicator presented in this script tracks several key volatility indices, including the VIX (S&P 500), GVZ (Gold), OVX (Crude Oil), and others, to help identify periods of increased uncertainty that could signal potential market turning points.

Volatility Indices and Their Relevance

Volatility indices like the VIX are considered “fear gauges” as they reflect the market’s expectation of future volatility derived from the pricing of options. A rising VIX typically signals increasing investor uncertainty and fear, which often precedes market corrections or significant price movements. In contrast, a falling VIX may suggest complacency or confidence in continued market stability (Whaley, 2000).

The other volatility indices incorporated in the indicator script, such as the GVZ (Gold Volatility Index) and OVX (Oil Volatility Index), capture the market’s perception of volatility in specific asset classes. For instance, GVZ reflects market expectations for volatility in the gold market, which can be influenced by factors such as geopolitical instability, inflation expectations, and changes in investor sentiment toward safe-haven assets. Similarly, OVX tracks the implied volatility of crude oil options, which is a crucial factor for predicting price movements in energy markets, often driven by geopolitical events, OPEC decisions, and supply-demand imbalances (Pindyck, 2004).

Using the Indicator to Identify Market Movements

The volatility indicator alerts traders when specific volatility indices exceed a defined threshold, which may signal a change in market sentiment or an upcoming price movement. These thresholds, set by the user, are typically based on historical levels of volatility that have preceded significant market changes. When a volatility index exceeds this threshold, it suggests that market participants expect greater uncertainty, which often correlates with increased price volatility and the possibility of a trend reversal.

For example, if the VIX exceeds a pre-determined level (e.g., 30), it could indicate that investors are anticipating heightened volatility in the equity markets, potentially signaling a downturn or correction in the broader market. On the other hand, if the OVX rises significantly, it could point to an upcoming sharp movement in crude oil prices, driven by changing market expectations about supply, demand, or geopolitical risks (Geman, 2005).

Practical Application

To effectively use this volatility indicator in market analysis, traders should monitor the alert signals generated when any of the volatility indices surpass their thresholds. This can be used to identify periods of market uncertainty or potential market turning points across different sectors, including equities, commodities, and currencies. The indicator can help traders prepare for increased price movements, adjust their risk management strategies, or even take advantage of anticipated price swings through options trading or volatility-based strategies (Black & Scholes, 1973).

Traders may also use this indicator in conjunction with other technical analysis tools to validate the potential for significant market movements. For example, if the VIX exceeds its threshold and the market is simultaneously approaching a critical technical support or resistance level, the trader might consider entering a position that capitalizes on the anticipated price breakout or reversal.

Conclusion

This volatility indicator is a robust tool for identifying market conditions that are conducive to significant price movements. By tracking the behavior of key volatility indices, traders can gain insights into the market’s expectations of future price fluctuations, enabling them to make more informed decisions regarding market entries and exits. Understanding and monitoring volatility can be particularly valuable during times of heightened uncertainty, as changes in volatility often precede substantial shifts in market direction (French et al., 1987).

References

• Bollerslev, T. (1986). Generalized Autoregressive Conditional Heteroskedasticity. Journal of Econometrics, 31(3), 307-327.

• Christoffersen, P. F. (1998). Evaluating Interval Forecasts. International Economic Review, 39(4), 841-862.

• Whaley, R. E. (2000). Derivatives on Market Volatility. Journal of Derivatives, 7(4), 71-82.

• Pindyck, R. S. (2004). Volatility and the Pricing of Commodity Derivatives. Journal of Futures Markets, 24(11), 973-987.

• Geman, H. (2005). Commodities and Commodity Derivatives: Modeling and Pricing for Agriculturals, Metals and Energy. John Wiley & Sons.

• Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3), 637-654.

• French, K. R., Schwert, G. W., & Stambaugh, R. F. (1987). Expected Stock Returns and Volatility. Journal of Financial Economics, 19(1), 3-29.

Bull / Bear Market RegimeBull / Bear Market Regime

Instructions:

- A simple risk on or risk off indicator based on CBOE's Implied Correlation and VIX to highlight and indicate Bull / Bear Markets. To be used with the S&P500 index as that's the source from where the CBOE calculates and measures implied volatility & implied correlation. Can also be used with the other indices such as: Dow Jones, S&P 500, Nasdaq, & Nasdaq100, & Index ETF's such as DIA, SPY, QQQ, etc.

- Know the active regime, see the larger picture using the Daily or Weekly view, and visualize the current "Risk On (Bull) or Risk Off (Bear)" environment.

Description:

- Risk On and Risk Off simplified & visualized. Know if we are in a RISK ON or RISK OFF environment (Bull or Bear Market). (Absolute bottoms and tops will occur BEFORE a Risk On (Bull Market) or Risk Off (Bear Market) environment is confirmed!) This indicator is not meant to bottom tick or uptick market price action, but to show the active regime.

- Green: Bull Market, Risk On, low volatility, and low risk.

- Red: Bear Market, Risk Off, high volatility, and higher risk.

Buy & Sell Indicators (DAILY time frame)

- Nothing is 100% guaranteed! Can be used for short to medium term trades at the users discretion in BEAR MARKETS!!

- These signals are meant to be used during a RISK OFF / BEAR MARKET environment that tends to be accompanied with high volatility. A Risk on / Bull Market environment tends to have low volatility and endless rallies, so the signals will differ and in most instances not apply for Bull market / Risk on regime.

- The SELL signal will more often than not signal that a pullback is near in a BULL market and that a BMR-Bear Market Rally is almost over in a BEAR market.

- The BUY signal will have far more accuracy in a BEAR market-high volatility environment and can Identify short-term and major bottoms.

Always use proper sizing and risk management!

Volatility Regime NavigatorA guide to understanding VIX, VVIX, VIX9D, VVIX/VIX, and the Composite Risk Score

1. Purpose of the Indicator

This dashboard summarizes short-term market volatility conditions using four core volatility metrics.

It produces:

• Individual readings

• A combined Regime classification

• A Composite Risk Score (0–100)

• A simplified Risk Bucket (Bullish → Stress)

Use this to evaluate market fragility, drift potential, tail-risk, and overall risk-on/off conditions.

This is especially useful for intraday ES/NQ trading, expected-move context, and understanding when breakouts or fades have edge.

2. The Four Core Volatility Inputs

(1) VIX — Baseline Equity Volatility

• < 16: Complacent (easy drift-up, but watch for fragility)

• 16–22: Healthy, normal volatility → ideal trading conditions

• > 22: Stress rising

• > 26: Tail-risk / risk-off environment

(2) VIX9D — Short-Term Event Vol

Measures 9-day implied volatility. Reacts to immediate news/events.

• < 14: Strongly bullish (drift regime)

• 14–17: Bullish to neutral

• 17–20: Event risk building

• > 20: Short-term stress / caution

(3) VVIX — Volatility of VIX (fragility index)

Tracks volatility of volatility.

• < 100: “Bullish, Bullish” — very low fragility

• 100–120: Normal

• 120–140: Fragile

• > 140: Stress, hedging pressure

(4) VVIX/VIX Ratio — Microstructure Risk-On/Risk-Off

One of the most sensitive indicators of market confidence.

• 5.0–6.5: Strongest “normal/bullish” zone

• < 5.0: Bottom-stalking / fear regime

• > 6.5: Complacency → vulnerable to reversals

• > 7.5: Fragile / top-risk

3. Composite Risk Score (0–100)

The dashboard converts all four inputs into a single score.

Score Interpretation

• 80–100 → Bullish - Drift regime. Shallow pullbacks. Upside favored.

• 60–79 → Normal - Healthy tape. Balanced two-way trading.

• 40–59 → Fragile - Choppy, failed breakouts, thinner liquidity.

• 20–39 → Risk-Off - Downside tails active. Favor fades and defensive behavior.

• < 20 → Stress - Crisis or event-driven tape. Avoid longs.

Score updates every bar.

4. Regime Label

Independent of the composite score, the script provides a Regime classification based on combinations of VIX + VVIX/VIX:

• Bullish+ → Buying is easy, tape lifts passively

• Normal → Cleanest and most tradable conditions

• Complacent → Top-risk; be careful chasing upside

• Mixed → Signals conflict; chop potential

• Bottom Stalk → High VIX, low VVIX/VIX (capitulation signatures)

A trailing “+” or “*” indicates additional bullish or caution overlays from VIX9D/VVIX.

5. How to Use the Dashboard in Trading

When Bullish (Score ≥ 80):

• Expect drift-up behavior

• Downside limited unless catalyst hits

• Structure favors breakouts and trend continuation

• Mean reversion trades have lower expectancy

When Normal (Score 60–79):

• The “playbook regime”

• Breakouts and mean reversion both valid

• Best overall trading environment

When Fragile (Score 40–59):

• Expect chop

• Breakouts fail

• Take quicker profits

• Avoid overleveraged directional bets

When Risk-Off (20–39):

• Favor fades of strength

• Downside tails activate

• Trend-following short setups gain edge

• Respect volatility bands

When Stress (<20):

• Avoid long exposure

• Do not chase dips

• Expect violent, news-sensitive behavior

• Position sizing becomes critical

6. Quick Summary

• VIX = weather

• VIX9D = short-term storm radar

• VVIX = foundation stability

• VVIX/VIX = confidence vs fragility

• Composite Score = overall regime health

• Risk Bucket = simple “what do I do?” label

This dashboard gives traders a high-confidence, low-noise view of equity volatility conditions in real time.

Historical VolatilityHistorical Volatility Indicator with Custom Trading Sessions

Overview

This indicator calculates **annualized Historical Volatility (HV)** using logarithmic returns and standard deviation. Unlike standard HV indicators, this version allows you to **customize trading sessions and holidays** for different markets, ensuring accurate volatility calculations for options pricing and risk management.

Key Features

✅ Custom Trading Sessions - Define multiple trading sessions per day with precise start/end times

✅ Multiple Markets Support - Pre-configured for US, Russian, European, and crypto markets

✅ Clearing Periods Handling - Account for intraday clearing breaks

✅ Flexible Calendar - Set trading days per year for different countries

✅ All Timeframes - Works correctly on intraday, daily, weekly, and monthly charts

✅ Info Table - Optional display showing calculation parameters

How It Works

The indicator uses the classical volatility formula:

σ_annual = σ_period × √(periods per year)

Where:

- σ_period = Standard deviation of logarithmic returns over the specified period

- Periods per year = Calculated based on actual trading time (not calendar time)

Calculation Method

1. Computes log returns: ln(close / close )

2. Calculates standard deviation over the lookback period

3. Annualizes using the square root rule with accurate period count

4. Displays as percentage

Settings

Calculation

- Period (default: 10) - Lookback period for volatility calculation

Trading Schedule

- Trading Days Per Year (default: 252) - Number of actual trading days

- USA: 252

- Russia: 247-250

- Europe: 250-253

- Crypto (24/7): 365

- Trading Sessions - Define trading hours in format: `hh:mm:ss-hh:mm:ss, hh:mm:ss-hh:mm:ss`

Display

- Show Info Table - Shows calculation parameters in real-time

Market Presets

United States (NYSE/NASDAQ)

Trading Sessions: 09:30:00-16:00:00

Trading Days Per Year: 252

Trading Minutes Per Day: 390

Russia (MOEX)

Trading Sessions: 10:00:00-14:00:00, 14:05:00-18:40:00

Trading Days Per Year: 248

Trading Minutes Per Day: 515

Europe (LSE)

Trading Sessions: 08:00:00-16:30:00

Trading Days Per Year: 252

Trading Minutes Per Day: 510

Germany (XETRA)

Trading Sessions: 09:00:00-17:30:00

Trading Days Per Year: 252

Trading Minutes Per Day: 510

Cryptocurrency (24/7)

Trading Sessions: 00:00:00-23:59:59

Trading Days Per Year: 365

Trading Minutes Per Day: 1440

Use Cases

Options Trading

- Compare HV vs IV - Historical volatility compared to implied volatility helps identify mispriced options

- Volatility mean reversion - Identify when volatility is unusually high or low

- Straddle/strangle selection - Choose optimal strikes based on historical movement

Risk Management

- Position sizing - Adjust position size based on current volatility

- Stop-loss placement - Set stops based on expected price movement

- Portfolio volatility - Monitor individual asset volatility contribution

Market Analysis

- Regime identification - Detect transitions between low and high volatility environments

- Cross-market comparison - Compare volatility across different assets and markets

Why Accurate Trading Hours Matter

Standard HV indicators assume 24-hour trading or use simplified day counts, leading to significant errors in annualized volatility:

- 5-minute chart error : Can be off by 50%+ if using wrong period count

- Options pricing impact : Even 2-3% HV error affects option values substantially

- Intraday vs overnight : Correctly excludes non-trading periods

This indicator ensures your HV calculations match the methodology used in professional options pricing models.

Technical Notes

- Uses actual trading minutes, not calendar days

- Handles multiple clearing periods within a single trading day

- Properly scales volatility across all timeframes

- Logarithmic returns for more accurate volatility measurement

- Compatible with Pine Script v6

Author Notes: This indicator was designed specifically for options traders who need precise volatility measurements across different global markets. The customizable trading sessions ensure your HV calculations align with actual market hours and industry-standard options pricing models.

ATR Future Movement Range Projection

The "ATR Future Movement Range Projection" is a custom TradingView Pine Script indicator designed to forecast potential price ranges for a stock (or any asset) over short-term (1-month) and medium-term (3-month) horizons. It leverages the Average True Range (ATR) as a measure of volatility to estimate how far the price might move, while incorporating recent momentum bias based on the proportion of bullish (green) vs. bearish (red) candles. This creates asymmetric projections: in bullish periods, the upside range is larger than the downside, and vice versa.

The indicator is overlaid on the chart, plotting horizontal lines for the projected high and low prices for both timeframes. Additionally, it displays a small table in the top-right corner summarizing the projected prices and the percentage change required from the current close to reach them. This makes it useful for traders assessing potential targets, risk-reward ratios, or option strategies, as it combines volatility forecasting with directional sentiment.

Key features:

- **Volatility Basis**: Uses weekly ATR to derive a stable daily volatility estimate, avoiding noise from shorter timeframes.

- **Momentum Adjustment**: Analyzes recent candle colors to tilt projections toward the prevailing trend (e.g., more upside if more green candles).

- **Time Horizons**: Fixed at 1 month (21 trading days) and 3 months (63 trading days), assuming ~21 trading days per month (excluding weekends/holidays).

- **User Adjustable**: The ATR length/lookback (default 50) can be tweaked via inputs.

- **Visuals**: Green/lime lines for highs, red/orange for lows; a semi-transparent table for quick reference.

- **Limitations**: This is a probabilistic projection based on historical volatility and momentum—it doesn't predict direction with certainty and assumes volatility persists. It ignores external factors like news, earnings, or market regimes. Best used on daily charts for stocks/ETFs.

The indicator doesn't generate buy/sell signals but helps visualize "expected" ranges, similar to how implied volatility informs option pricing.

### How It Works Step-by-Step

The script executes on each bar update (typically daily timeframe) and follows this logic:

1. **Input Configuration**:

- ATR Length (Lookback): Default 50 bars. This controls both the ATR calculation period and the candle count window. You can adjust it in the indicator settings.

2. **Calculate Weekly ATR**:

- Fetches the ATR from the weekly timeframe using `request.security` with a length of 50 weeks.

- ATR measures average price range (high-low, adjusted for gaps), representing volatility.

3. **Derive Daily ATR**:

- Divides the weekly ATR by 5 (approximating 5 trading days per week) to get an equivalent daily volatility estimate.

- Example: If weekly ATR is $5, daily ATR ≈ $1.

4. **Define Projection Periods**:

- 1 Month: 21 trading days.

- 3 Months: 63 trading days (21 × 3).

- These are hardcoded but based on standard trading calendar assumptions.

5. **Compute Base Projections**:

- Base projection = Daily ATR × Days in period.

- This gives the total expected movement (range) without direction: e.g., for 3 months, $1 daily ATR × 63 = $63 total range.

6. **Analyze Candle Momentum (Win Rate)**:

- Counts green candles (close > open) and red candles (close < open) over the last 50 bars (ignores dojis where close == open).

- Total colored candles = green + red.

- Win rate = green / total colored (as a fraction, e.g., 0.7 for 70%). Defaults to 0.5 if no colored candles.

- This acts as a simple momentum proxy: higher win rate implies bullish bias.

7. **Adjust Projections Asymmetrically**:

- Upside projection = Base projection × Win rate.

- Downside projection = Base projection × (1 - Win rate).

- This skews the range: e.g., 70% win rate means 70% of the total range allocated to upside, 30% to downside.

8. **Calculate Projected Prices**:

- High = Current close + Upside projection.

- Low = Current close - Downside projection.

- Done separately for 1M and 3M.

9. **Plot Lines**:

- 3M High: Solid green line.

- 3M Low: Solid red line.

- 1M High: Dashed lime line.

- 1M Low: Dashed orange line.

- Lines extend horizontally from the current bar onward.

10. **Display Table**:

- A 3-column table (Projection, Price, % Change) in the top-right.

- Rows for 1M High/Low and 3M High/Low, color-coded.

- % Change = ((Projected price - Close) / Close) × 100.

- Updates dynamically with new data.

The entire process repeats on each new bar, so projections evolve as volatility and momentum change.

### Examples

Here are two hypothetical examples using the indicator on a daily chart. Assume it's applied to a stock like AAPL, but with made-up data for illustration. (In TradingView, you'd add the script to see real outputs.)

#### Example 1: Bullish Scenario (High Win Rate)

- Current Close: $150.

- Weekly ATR (50 periods): $10 → Daily ATR: $10 / 5 = $2.

- Last 50 Candles: 35 green, 15 red → Total colored: 50 → Win Rate: 35/50 = 0.7 (70%).

- Base Projections:

- 1M: $2 × 21 = $42.

- 3M: $2 × 63 = $126.

- Adjusted Projections:

- 1M Upside: $42 × 0.7 = $29.4 → High: $150 + $29.4 = $179.4 (+19.6%).

- 1M Downside: $42 × 0.3 = $12.6 → Low: $150 - $12.6 = $137.4 (-8.4%).

- 3M Upside: $126 × 0.7 = $88.2 → High: $150 + $88.2 = $238.2 (+58.8%).

- 3M Downside: $126 × 0.3 = $37.8 → Low: $150 - $37.8 = $112.2 (-25.2%).

- On the Chart: Green/lime lines skewed higher; table shows bullish % changes (e.g., +58.8% for 3M high).

- Interpretation: Suggests stronger potential upside due to recent bullish momentum; useful for call options or long positions.

#### Example 2: Bearish Scenario (Low Win Rate)

- Current Close: $50.

- Weekly ATR (50 periods): $3 → Daily ATR: $3 / 5 = $0.6.

- Last 50 Candles: 20 green, 30 red → Total colored: 50 → Win Rate: 20/50 = 0.4 (40%).

- Base Projections:

- 1M: $0.6 × 21 = $12.6.

- 3M: $0.6 × 63 = $37.8.

- Adjusted Projections:

- 1M Upside: $12.6 × 0.4 = $5.04 → High: $50 + $5.04 = $55.04 (+10.1%).

- 1M Downside: $12.6 × 0.6 = $7.56 → Low: $50 - $7.56 = $42.44 (-15.1%).

- 3M Upside: $37.8 × 0.4 = $15.12 → High: $50 + $15.12 = $65.12 (+30.2%).

- 3M Downside: $37.8 × 0.6 = $22.68 → Low: $50 - $22.68 = $27.32 (-45.4%).

- On the Chart: Red/orange lines skewed lower; table highlights larger downside % (e.g., -45.4% for 3M low).

- Interpretation: Indicates bearish risk; might prompt protective puts or short strategies.

#### Example 3: Neutral Scenario (Balanced Win Rate)

- Current Close: $100.

- Weekly ATR: $5 → Daily ATR: $1.

- Last 50 Candles: 25 green, 25 red → Win Rate: 0.5 (50%).

- Projections become symmetric:

- 1M: Base $21 → Upside/Downside $10.5 each → High $110.5 (+10.5%), Low $89.5 (-10.5%).

- 3M: Base $63 → Upside/Downside $31.5 each → High $131.5 (+31.5%), Low $68.5 (-31.5%).

- Interpretation: Pure volatility-based range, no directional bias—ideal for straddle options or range trading.

In real use, test on historical data: e.g., if past projections captured actual moves ~68% of the time (1 standard deviation for ATR), it validates the volatility assumption. Adjust the lookback for different assets (shorter for volatile cryptos, longer for stable blue-chips).

IV Rank Oscillator by dinvestorqShort Title: IVR OscSlg

Description:

The IV Rank Oscillator is a custom indicator designed to measure and visualize the Implied Volatility (IV) Rank using Historical Volatility (HV) as a proxy. This indicator helps traders determine whether the current volatility level is relatively high or low compared to its historical levels over a specified period.

Key Features :